One of the greatest injustices of modern Western politics is that the young are poorer than their parents were at the same age, because of political decisions made by their parent’s generation. My last article sparked a few indignant replies for pointing out the obscene welfare benefits millionaire Boomers are extracting from the British state. I’ve noticed that every time this topic comes up, the same excuses appear. So here, in one handy article, I present the seven great myths of Boomer entitlement.

House prices rose naturally

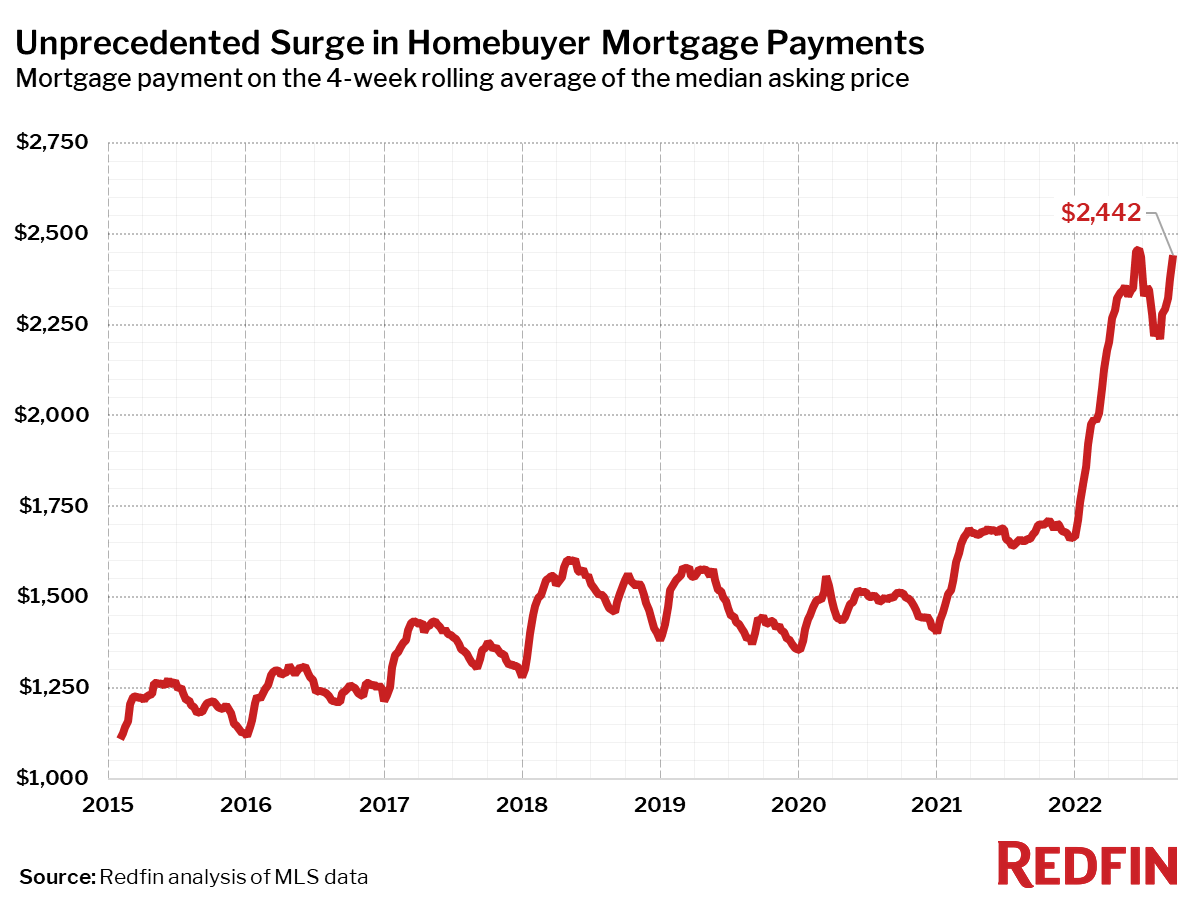

Price-to-income ratios have roughly doubled since the Boomer buying era. In 1985, during the peak Boomer buying years, the median home sold for $82,800 while median household income was $23,620 — a ratio of 3.5×. By 2025, the median home had reached $416,900 against $83,150 in median income — a 5× ratio, with homes up 403% and income up 252%.

")

The surge came from deliberate supply restrictions (NIMBY zoning enforced by older homeowners), loose monetary policy that inflated assets, mass immigration driving up demand that couldn’t be met, and Boomers refusing to downsize en masse. Boomers now sit on trillions in home equity precisely because the system they created made housing a speculative store of value, and because each successive generation has faced a higher barrier to entry.

As a result, empty-nest Boomers in the U.S. now own nearly twice the share of large homes as Millennial families. In the UK, over-60s own 55% of all property in the UK, with those under 40 owning just 10%.

Boomers faced 15% mortgage rates

Boomers will sometimes cite historically high interest rates in the early 1980s, but it’s meaningless given that they still translated to mortgage payments that are a fraction of what this generation pays. Boomers bought at price-to-income ratios of roughly 3–3.5×. They then enjoyed multiple tailwinds the next generations never received:

Rates fell sharply through the 1980s and 1990s and gave them easy refinancing.

High inflation wiped out the real value of their fixed-rate debt.

Decades of strong house-price appreciation turned modest purchases into massive equity.

What does the nominal interest rate matter when the relative burden was far lighter and the equity gains were locked in for decades?

Young people are irresponsible with their money

Gen Z are actually saving for retirement more than Gen X and Boomers did. Gen Z start saving for retirement at a median age of 22, about 13 years earlier than Baby Boomers or Gen X.

This is despite the aforementioned 2–3× higher housing costs relative to wages, higher student debt, and decades of stagnant real wage growth.

Boomers entered adulthood with cheap homes, near-free college, affordable living, a low number of dependent pensioners relative to the working-age population, strong unions, and they were on the cusp of a historic, multi-decade explosion in wealth from which they could benefit through even modest asset ownership.

Pensioners paid into a pot — it’s their money

This is the biggest lie told by defenders of gerontocracy. Across the West, state pensions are overwhelmingly pay-as-you-go. All your “contributions” were spent on the previous generation’s pensions, and there is no ring-fenced personal pot earning returns for you. Current workers fund current retirees.

People are so brazen with this lie that someone commented under my previous post on Britain’s triple lock policy that I “seem to forget that they paid into the system all their working lives and many retired people don’t get the full State Pension. It’s not free money.”

Remember, this is in defence of a policy where state pensions are automatically upgraded every year by whichever is highest: inflation, average earnings growth, or 2.5%. The system is actually designed to ensure pension gains outpace average earnings growth, and its defenders still frame it as honouring some kind of fixed obligation.

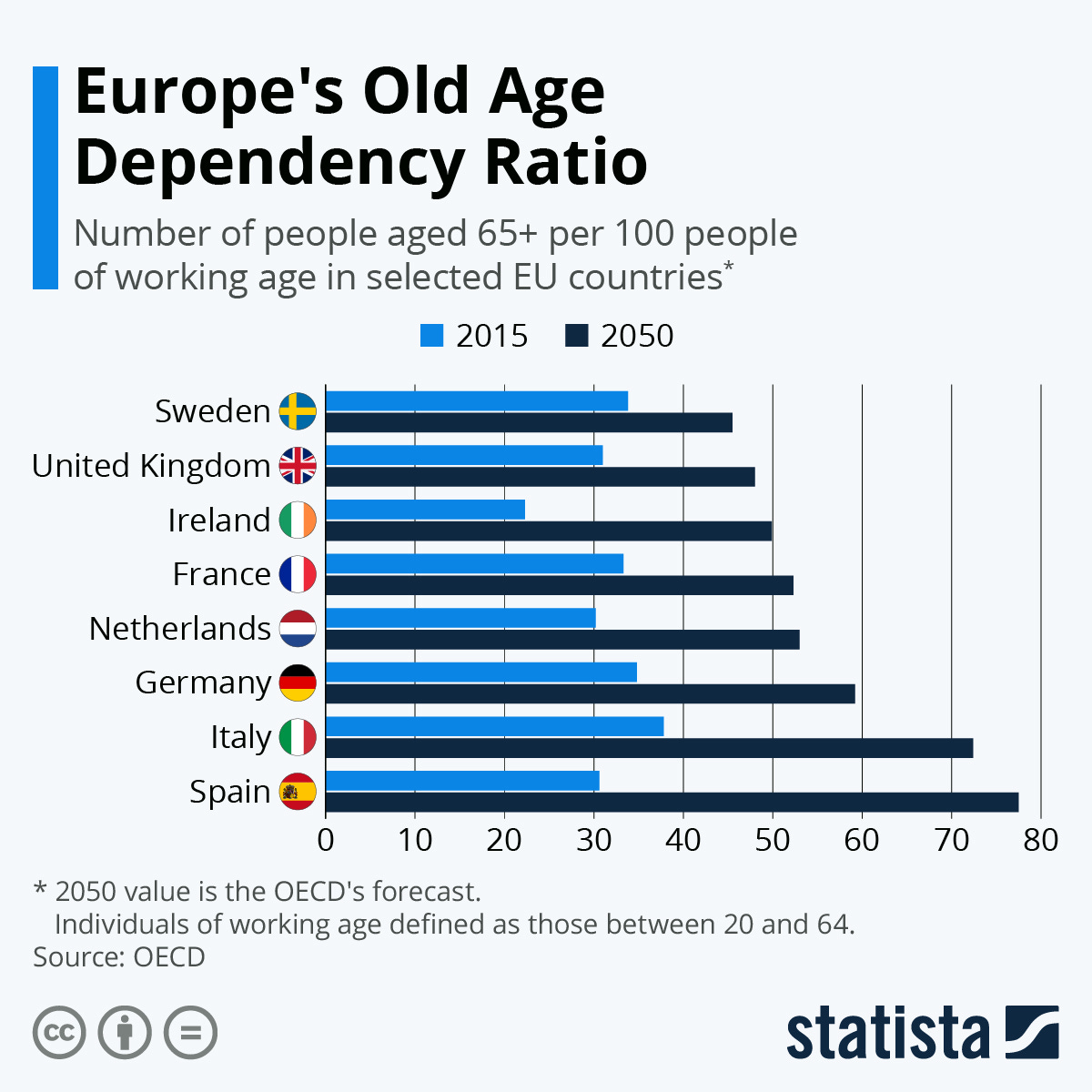

Baby Boomers did not pay into a future pension pot. When they funded the state during their peak working years, the worker-to-beneficiary ratio was far higher — around 3–5 workers per retiree through the 1970s–1990s. There are 2.7 workers for every pensioner in America today, a ratio similar to the UK. In Germany the old-age dependency ratio set to increase to 51% by 2050; Italy will be over 66% by that point.

This is a massive intergenerational transfer from a shrinking pool of younger workers to a much larger, longer-living cohort of retirees, and a complete inversion of the favourable demographics Boomers enjoyed when they were paying in.

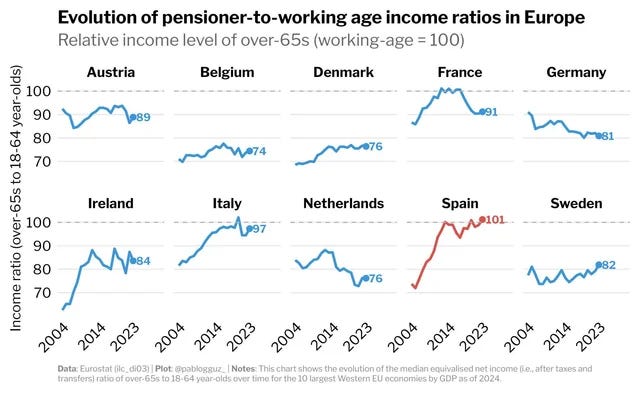

The result is visible across Europe. In several major economies, pensioners now have net incomes approaching those of working-age adults; in some countries like Spain, they are slightly higher:

The young will get it all through inheritance anyway

The same commenter who said Boomers had funded their own pensions commented that I should remember that “this wealth will trickle down to the next generation and that will give them a head start.”

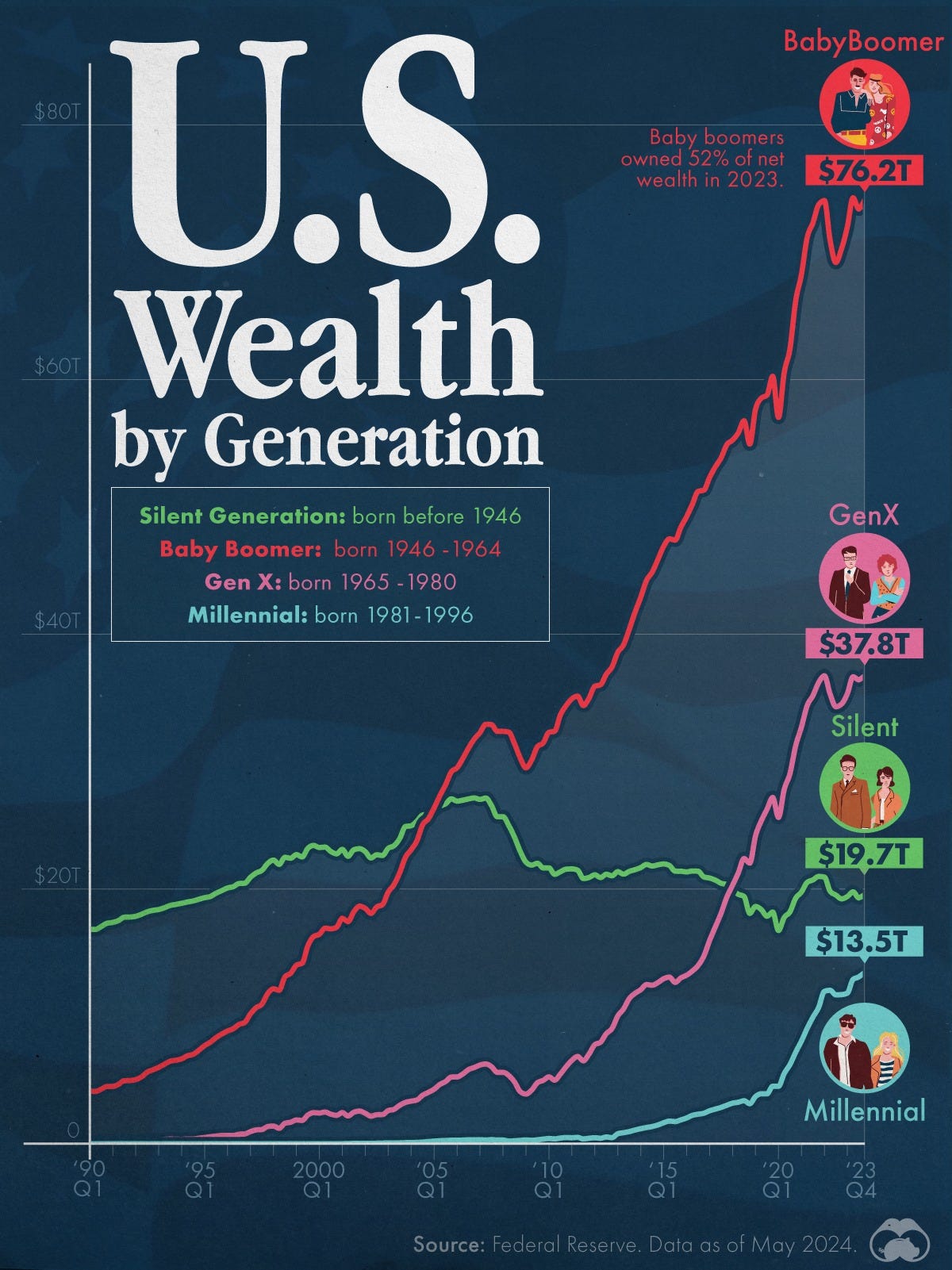

There will be a great wealth transfer eventually but most will never see this. Boomers hold ~half of national wealth, and many are ready to spend it on long retirements, healthcare, and comfortably leisurely lifestyles. Inheritances arrive late (typical recipient in their 50s–60s), well after the point where they could have aided family formation and other milestones for the next generation.

The transfer is also extremely unequal. It’s ridiculous to point to a minority receiving large inheritances, usually late in life, and act like this corrects a structural imbalance that affects every subsequent generation.

Not only that, but Boomers believe less in passing on their wealth to their children than any generation to ever exist! They explicitly say they plan to enjoy their money or leave less than expected. Just look at how many famous Boomer celebrities have bragged about the promise of leaving nothing to their children.

A survey reported last year found that only 22% of Baby Boomers expect to leave an inheritance, and only half that number rated it a top priority.

Another survey found that only 21% of Boomers with at least $1 million in investable assets said they want the next generation to enjoy their wealth, compared to 53% of Millennials. Three times more Boomers than Millennials say they want to enjoy the money for themselves while alive. If someone thinks stereotypes about Boomer entitlement are unfair, show them this:

We must protect house prices for the good of the economy

This is the economics of gerontocracy. High house prices enrich current owners, who are disproportionately older, at the expense of labour mobility, entrepreneurship, family formation and new home ownership.

Turning housing from shelter into a speculative rentier asset creates (sometimes disastrous) bubbles, enables parasitic rent extraction, and locks national wealth into an unproductive asset which misallocates capital and stifles genuine economic growth.

This is not a neutral policy because all the policies that inflated Boomer assets were choices made at the cost of alternatives. In this context, “the good of the economy” just means protecting Boomer balance sheets at everyone else’s expense.

Pensioners are ‘asset rich, cash poor’ so we can’t tax their asset wealth or cut their benefits

Today’s retirees — especially Baby Boomers — are the wealthiest cohort in history. Boomers in the United States hold over half the country’s wealth.

Much of this wealth sits in housing. Most older homeowners are mortgage-free and sitting on massive unrealised gains created by decades of asset inflation downstream of policies that favoured them.

If they are genuinely “cash poor,” they have multiple straightforward options to unlock equity. The reason they don’t is that many simply choose not to. They prefer to preserve their full asset base while receiving universal benefits, public services subsidised by working-age taxpayers, and special tax protections.

The fact that pensioners have trillions tied up in unrealised gains is supposed to elicit great sympathy, but not the “cash poor” situation of younger workers who are paying rent, taxes and pension contributions with no realistic path to ownership. And of course, the same people invoking the “cash poor” excuse would oppose almost any policy designed to encourage retirees to make their wealth more liquid and free up the housing market.

My latest book, Ethnopolitics, is now available. The book collects 15 of my best essays on how collective identity shapes the world. Its two lengthiest essays are exclusive to the book, a study of the psychology of the left and the mental pathologies that drive extreme leftism, and an ethnohistory of the Norman people and the extraordinary mark they left on European history.

“Keith Woods is one of the most accomplished of a rising generation of ethnic nationalists. His new book Ethnopolitics demonstrates its relevance to a wide range of political issues, showing why ethnopolitics is the wave of the future. I highly recommend Ethnopolitics to all my readers.”

— Greg Johnson

Purchase Ethnopolitics in your preferred format and region on Amazon:

I'm a boomer but don't have a dog in this fight. One factor Mr. Woods might like to chew on is the lopsided allocation of government spending between the kids and the old people. There was a Governor of Colorado in the US who amazingly had the guts to talk about this. I forget his name. He pointed out that the government spent more on the last 6 months of life than on the first SIX YEARS of life. The reason? The elderly have the vote. Kids - for good reason - do not. No other species subordinates the interests of the chicks in the nest to the interests of the dying birds.

The ultimate proof of the boomer generation’s contempt for their children, their children’s children, and beyond, is the implementation of reverse mortgages. Most younger generations won’t even inherit their homes because they’ll be on foundations of severe debt they can’t take on or, even worse, won’t be allowed to take on. The worst part of it all is that many boomers don’t even see the consequences of this “free money” they receive by engaging in this practice (or they simply don’t care). Once the boomer generation dies out, most home properties will be the properties of banks. Banks will become the new landlords and it won’t be for the better.